The introduction of the Income-tax Act, 2025 has sparked widespread discussion among taxpayers across India. One of the biggest questions during the 2026 income tax return filing season is whether individuals will have to file two separate Income Tax Returns (ITRs) because of the transition from the familiar "Assessment Year" (AY) system to the newly introduced "Tax Year" concept.

The confusion is understandable. For decades, taxpayers have filed returns based on the Assessment Year, while the new legislation replaces this terminology with a simpler Tax Year framework from April 1, 2026. Many salaried employees, professionals, business owners, and pensioners assumed that this change could require filing one return under the old system and another under the new one.

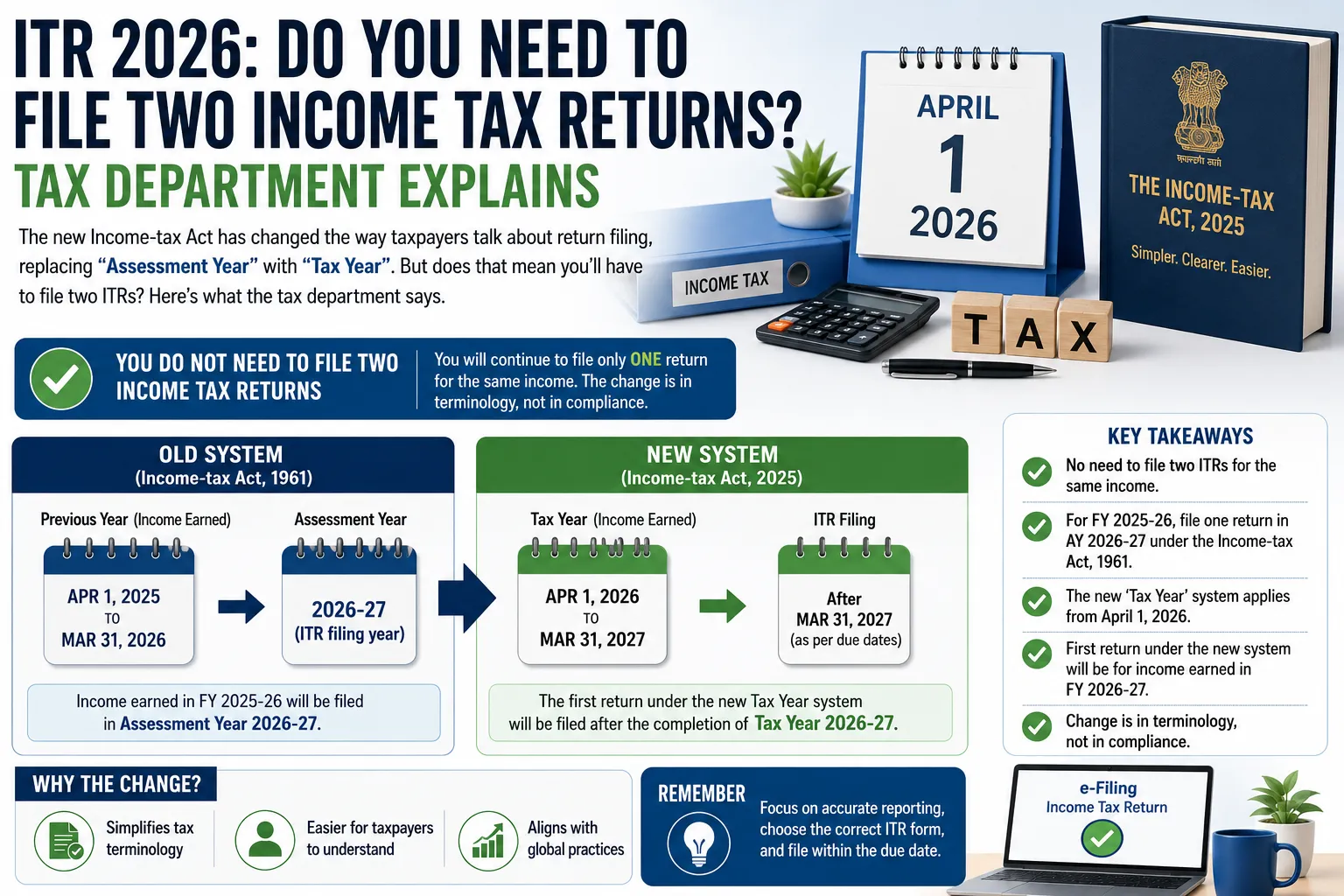

Fortunately, the Income Tax Department has clarified that taxpayers do not need to file two income tax returns for the same income. The transition is primarily a change in terminology and reporting structure rather than an additional compliance requirement. Understanding how this change works can help taxpayers avoid unnecessary confusion during the filing season.

Why the Confusion Began

The Income-tax Act, 2025 introduces several structural reforms aimed at simplifying India's tax laws. Among the most noticeable changes is replacing the long-used concepts of "Previous Year" and "Assessment Year" with a single term called "Tax Year."

Because the new Act came into force on April 1, 2026, many taxpayers assumed that both systems would operate simultaneously, requiring two separate return filings.

The Income Tax Department has officially clarified that this is not the case. Taxpayers filing returns for income earned during the Financial Year (FY) 2025-26 will continue to file only one return under Assessment Year 2026-27 as per the provisions of the Income-tax Act, 1961. The new Tax Year framework applies only to income earned from April 1, 2026 onwards.

What Is the Difference Between Assessment Year and Tax Year?

Under the previous system, taxpayers earned income during one financial year, known as the Previous Year, and filed their Income Tax Return in the following Assessment Year.

For example, income earned between April 1, 2025 and March 31, 2026 is reported in Assessment Year 2026-27.

Many taxpayers found this terminology confusing because the year in which income was earned differed from the year used for filing the return.

The new Income-tax Act seeks to simplify this process by replacing both "Previous Year" and "Assessment Year" with a single concept called "Tax Year."

Under the revised system, the Tax Year generally refers to the twelve-month period beginning on April 1 and ending on March 31, making it easier for taxpayers to understand the reporting period.

Why You Don't Need to File Two Returns

The most important clarification issued by the Income Tax Department is that taxpayers will not have to file duplicate returns for the same income.

If you earned income during FY 2025-26, you must file only one Income Tax Return under Assessment Year 2026-27.

There is no requirement to submit another return simply because the new Tax Year framework has been introduced.

Similarly, the first return under the Tax Year system will relate to income earned from April 1, 2026 to March 31, 2027 and will become due only after the completion of that Tax Year.

This ensures a smooth transition without creating additional compliance burdens.

Which Law Applies to FY 2025-26 Income?

Another common question concerns which law governs income earned before April 1, 2026.

Although taxpayers will file their returns after the new Income-tax Act has come into force, income earned during FY 2025-26 will continue to be governed by the Income-tax Act, 1961.

The reason is straightforward.

The relevant income period began before the commencement of the new legislation, meaning the earlier law continues to apply for that particular return.

This clarification removes uncertainty for millions of taxpayers preparing their annual returns.

When Will the Tax Year System Actually Begin?

The new Tax Year framework applies only to income earned from April 1, 2026 onwards.

Therefore, income generated between April 1, 2026 and March 31, 2027 will fall under Tax Year 2026-27.

However, taxpayers will not file this return immediately.

As with the earlier system, the return becomes due only after the completion of the relevant income period.

This means the first return under the Tax Year framework will be filed after March 31, 2027, according to the applicable due dates prescribed by the Income Tax Department.

Why the Government Introduced the Tax Year Concept

The primary objective behind introducing the Tax Year is simplification.

For many taxpayers, especially first-time filers, the distinction between Previous Year and Assessment Year often caused confusion.

Using a single Tax Year reduces unnecessary complexity while making tax compliance easier to understand.

The reform also aligns India's tax terminology more closely with international practices followed in several countries where tax reporting is linked directly to the income year itself.

Simpler terminology can improve taxpayer awareness and reduce filing errors over time.

What This Means for Salaried Employees

For salaried individuals, the transition requires very little change in the immediate filing season.

Employees will continue receiving Form 16 and other tax-related documents as usual for FY 2025-26.

While filing their return, they must select Assessment Year 2026-27 using the notified ITR forms applicable under the Income-tax Act, 1961.

There is no additional form, duplicate filing, or extra compliance because of the Tax Year transition.

Taxpayers should continue reconciling their income with Form 26AS, the Annual Information Statement (AIS), and other supporting documents before filing.

Choosing the Correct ITR Form

Even though the terminology is changing, taxpayers must still choose the correct Income Tax Return form based on their income profile.

Different forms are prescribed for salaried individuals, professionals, businesses, companies, trusts, and other categories of taxpayers.

Selecting the appropriate form remains essential because filing the wrong return may lead to processing delays or notices from the Income Tax Department.

Taxpayers should carefully review the eligibility conditions before filing.

Common Mistakes to Avoid

While the Tax Year transition has generated headlines, taxpayers should remain focused on accurate reporting rather than terminology alone.

Some common mistakes include reporting incorrect income, failing to disclose interest earnings, overlooking capital gains, claiming ineligible deductions, or not matching income details with AIS and Form 26AS.

Errors can delay refunds or trigger further verification by the Income Tax Department.

Reviewing all financial documents before filing remains one of the best ways to ensure smooth processing.

Benefits of the New System

Although taxpayers will notice little immediate change during the current filing season, the Tax Year concept offers several long-term advantages.

It simplifies communication between taxpayers and the department.

It reduces confusion created by multiple tax period names.

It makes tax education easier for new taxpayers.

It also provides greater consistency in future tax administration.

By removing overlapping terminology, the government hopes to create a more user-friendly tax compliance framework.

Preparing for Future Filing Seasons

The current filing season represents a transitional phase.

Taxpayers should familiarize themselves with the new Tax Year terminology while continuing to follow existing filing procedures for FY 2025-26.

Future filing seasons will gradually adopt the revised framework as income earned after April 1, 2026 becomes subject to the provisions of the Income-tax Act, 2025.

Staying informed about these changes will help taxpayers adapt smoothly without confusion.

Conclusion

The transition from the Assessment Year system to the new Tax Year framework has naturally raised questions among taxpayers, but the Income Tax Department has provided a clear and reassuring answer. There is no requirement to file two Income Tax Returns for the same income. Individuals earning income during FY 2025-26 will continue filing a single return for Assessment Year 2026-27 under the Income-tax Act, 1961, while the new Tax Year framework will apply only to income earned from April 1, 2026 onwards.

The introduction of the Tax Year is intended to simplify India's tax system rather than increase compliance. By replacing multiple reporting terms with a single, easy-to-understand concept, the government aims to make return filing more straightforward for millions of taxpayers. As long as taxpayers use the correct ITR form, verify their financial information carefully, and file within the prescribed deadlines, the transition should remain smooth and hassle-free.

islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub islamicduahub